Critical Illness Insurance Explained

Why consider Critical Illness Insurance?

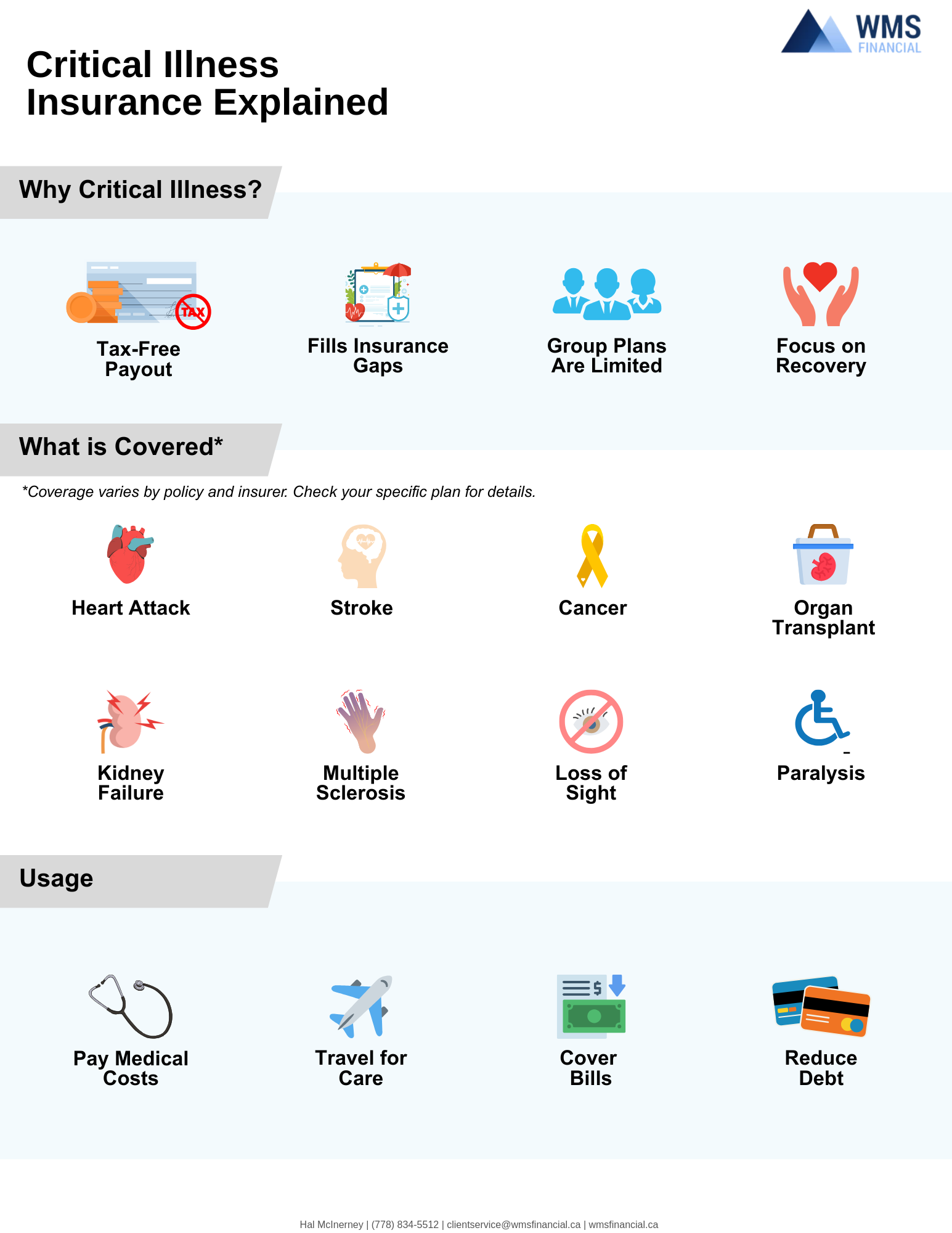

The purpose of Critical Illness Insurance is to provide a tax-free lump sum benefit if you’re diagnosed with a covered serious illness. It’s designed to ease the financial pressure that often comes with time away from work, medical costs not covered by government plans, and other unexpected expenses — so you can focus on your recovery, not your finances.

Even if you already have life insurance or workplace benefits, Critical Illness Insurance offers unique protection. Group plans often include only small amounts of coverage, may end if you leave your job, and usually don’t let you choose the benefit amount. A personal policy stays with you and can be tailored to your needs.

What does it cover?

Critical Illness Insurance pays out if you’re diagnosed with one of the serious medical conditions listed in your policy. These commonly include:

- Cancer

- Heart attack

- Stroke

- Major organ transplant

- Kidney failure

- Multiple sclerosis

- Paralysis, loss of sight, hearing, or limbs

- Alzheimer’s, Parkinson’s, motor neuron disease

- Severe burns, benign brain tumour, aortic surgery

Some policies also provide partial payments for early-stage diagnoses. Your advisor can explain the specific definitions and conditions covered by your plan.

What types of policies are available?

Critical Illness Insurance is available in several forms, so you can choose the one that fits your needs and budget. The most common types include:

- Term policies: Coverage for a fixed period, such as 10, 20, or 25 years.

- Permanent policies: Coverage that lasts for life, as long as you pay the premiums.

- Return of premium policies: Refund some or all premiums if no claim is made.

- Group plans through an employer: Limited and usually not portable.

Is there a waiting period?

Yes — most policies include a short waiting period after diagnosis, usually 30 days, before the benefit is paid.

What factors affect the cost of Critical Illness Insurance?

The premium you pay for Critical Illness Insurance is influenced by both your personal situation and the policy you select. Understanding these factors can help you plan your coverage effectively:

- Age: Younger applicants generally pay lower premiums, since the risk of serious illness increases with age.

- Health history: Your medical history, as well as your family history, may lead to higher premiums or exclusions if there are risk factors.

- Gender: Rates can differ slightly between men and women because of different incidence rates for certain conditions.

- Smoking status: Smokers face higher premiums because of significantly greater risks of illnesses like cancer, heart disease, and stroke.

- Lifestyle and occupation: Risky hobbies or high-stress, physically demanding jobs can also impact your cost.

- Coverage amount: The larger the lump sum benefit you choose, the higher your premium.

- Policy term: Permanent policies tend to cost more than term policies with fixed durations.

- Optional riders: Adding features such as return of premium, premium waivers, or child coverage increases your premium.

By working with an advisor, you can balance these factors and find a policy that gives you the right level of protection at a price you’re comfortable with.

Are the benefits taxable?

No — in Canada, Critical Illness Insurance pays a tax-free lump sum benefit you can use however you wish.

How can you use the money?

The benefit is completely flexible. Many use it to:

- Cover household expenses while off work

- Pay for medications or private care

- Reduce debts

- Compensate a caregiver’s lost income

- Travel for specialized treatment

When is the best time to purchase?

The best time to purchase Critical Illness Insurance is when you’re younger and healthy, so you qualify more easily and pay lower premiums.

How does Critical Illness Insurance fit into your insurance plan?

Most people already include life insurance in their plans to protect their family if they pass away. Many also rely on group disability insurance to replace part of their income if they can’t work due to illness or injury.

But Critical Illness Insurance is often overlooked — and that can leave a gap.

Life insurance only pays if you die, and disability insurance often replaces only a portion of your income, usually with limits and waiting periods. Neither addresses the immediate, unexpected costs of a serious illness, like out-of-pocket medical expenses, travel for treatment, hiring help at home, or paying off debts quickly.

Critical Illness Insurance fills this gap by providing a lump sum, tax-free benefit right after diagnosis, even if you’re still able to work. It complements your life and disability insurance to give you and your family a more complete, well-rounded safety net.

It’s worth reviewing your overall plan to make sure all three pieces — life, disability, and critical illness — are working together to protect your family and your lifestyle no matter what happens.

Critical Illness Insurance provides financial security during one of life’s most challenging times. It’s flexible, tax-free, and tailored to your needs — giving you and your family confidence that you’ll have support if the unexpected happens.

If you’d like help exploring your options or getting a personalized quote, reach out anytime.